Stabilizing the Economy: The Role of the Fed

Fed and Monetary Policy

- Stabilization policies are govt policies affecting Planned Aggregate Expenditures

- Conducting monetary policy is Fed’s primary task

- Monetary policy is quick and responsive tool as it can be changed by FOMC, while fiscal policy can only be changed by legislative action

- FOMC changes money supply through monetary policy changes by modifying short-term nominal interest rates, or the Federal Funds Rate

- This is equivalent to setting the money supply since

- Value of money supply implies given nominal interest rate

- Vale of nominal interest rate implies given money supply

- Nominal interest rate is opportunity cost of holding money

Fed and Interest Rates: Basic Model

- Demand for money is amount of wealth a nation’s people wish to hold in form of money

- Equilibrium in money market (i.e money supply = money demand) determines equilibrium nominal interest rate, equilibrium money supply/demand

National Demand for Money

- Nominal interest rate (i) - negative relationship

- Higher interest rate, higher opp. cost of holding money, so lower demand for money

- Real income or output (Y) - positive relationship

- Higher income, greater quantity of money demanded

- Price level (P) - positive relationship

- Higher price level, greater quantity of money demanded

- Rightward shift in demand curve for money can be caused by

- Increase in real GDP

- Increase in price level

- Tech. changes/improvements

- Increase in foreign demand for dollars

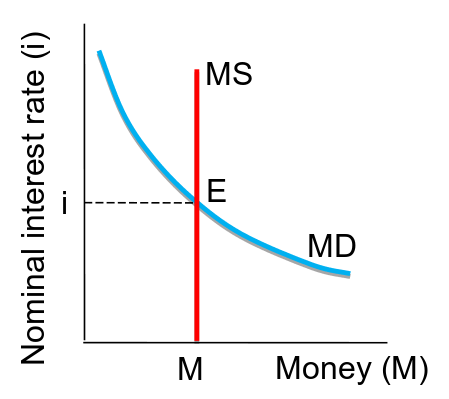

Supply of Money

- Fed primarily controls money supply with open market operations

- Supply of money is vertical line in figure below

- Fed wants to increase money supply to new M′

- This establishes a new equilibrium with lower interests, convincing market to hold the new larger amount of money

Money supply

Money supply

Fed Targets Interest Rate

- Sets interest rate because closely tied to bank reserve levels

- Policy also announced in interest rate because

- Public not familiar with “money supply”

- Interest rate affects planned spending and level of economic activity

- Interests rates easier to monitor than money supply itself

- The Fed can control real interest rates in the short run

- Inflation does not adjust very quickly, and real interest rate r=i−π, where π is inflation rate, so i has heavy impact on r

- But over long run inflation rate will change

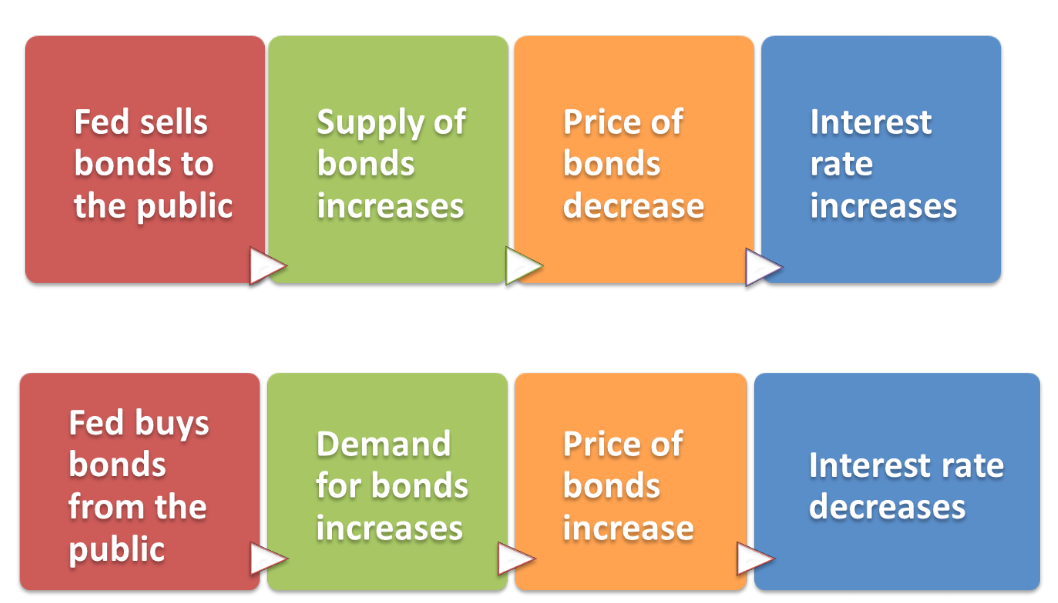

Fed bond control

Fed bond control

Excess Reserves

- Banks could hold excess reserves (reserve amounts above legal minimum), reducing Fed’s ability to control money supply through open market operations

- Banks might hold these reserves in times of uncertainty

Quantitative Easing

- Quantitative easing is expansionary monetary policy where Fed buys long-term financial assets (like mortgage back securities, long term treasuries)

- Goal is to increase long-term interest rates, as they don’t always move with the Federal Funds Rate

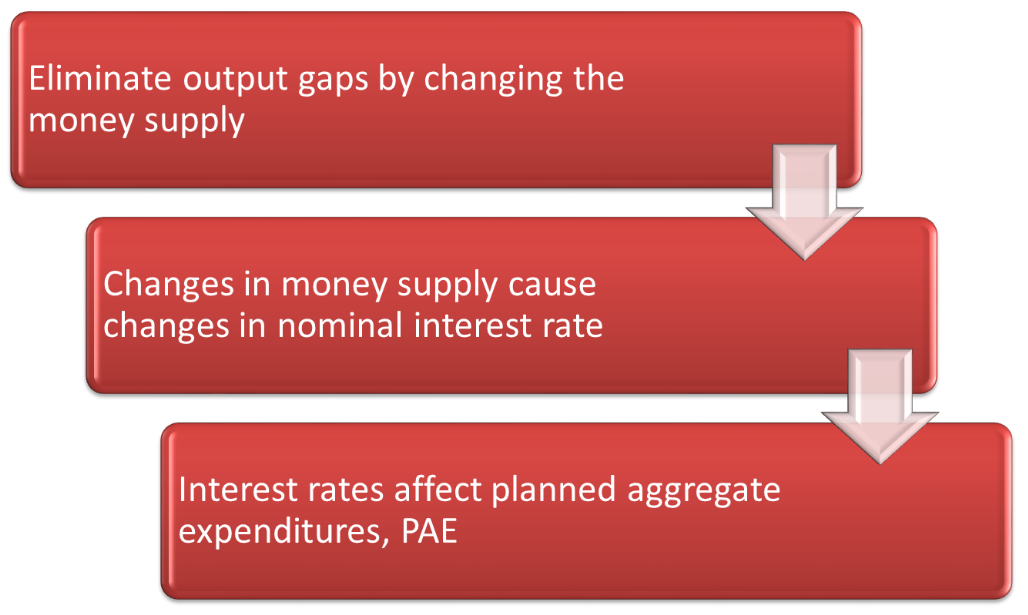

The Fed and the Economy

Fed and economics

Fed and economics

Monetary Policy

Monetary policy 1

Monetary policy 1

Monetary policy 2

Monetary policy 2

Fed Fights Inflation

- Expansionary gaps can lead to inflation

- Fed tries to close these gaps by raising interest rates, causing a decrease in consumption, PAE, and equilibrium output’

Inflation and the Stock Market

- Bad news about inflation generally causes stock prices to fall

- Investors anticipate Fed will increase interest rates, meaning

- Economic activity slows, lowering firm’s sales and potentially profits

- Higher interest rates makes non-stock financial instruments more attractive

- Reduces demand for stocks and thus their price drops

Fed and Stock Market

- Has limited ability to manage stock market

- Monetary policy not well suited to addressing asset bubble (increase in asset price over their market values)

- Fed could slow economy and raise interest rates, but might result in recession

Taylor’s Rule

- Describes Fed’s behavior, so called policy reaction function

- Written as r=0.01+0.5Y∗Y−Y∗+0.5π where r is real interest rate and the fraction is output proportional to potential GDP

- Maps inflation rate π and output gap to real interest rate that Fed should set

- Useful simplifying assumption is that Fed’s choice of real interest rate depends only on rate of inflation